A fiscal pattern is used to define date formats and calculations in relation to your how your

organization has defined its fiscal calendar. Fiscal patterns divide fiscal years into periods

(usually quarters), and then define the number of weeks for each of the three months that fall

within. All fiscal patterns rely on a fixed calendar date from which all past and future dates

and calculations are based. However, a fiscal pattern's start date and a fiscal calendar's

start date do not need to be identical. Fiscal patterns generally do not account for one or

two days per year (depending on leap years); an additional week is periodically added to the

final month (typically January) to account for the extra days.

The format for defining a fiscal pattern is a comma delimited row of 12 digits (or 13, if

your organization's fiscal calendar has 13 periods). Commas separate each quarter in the

fiscal year. Rows separate each fiscal year. Each digit in a row represents the number of

weeks in a month for the position of the month in the fiscal pattern. The number of weeks in a

month used in the fiscal pattern should match the number of weeks that have already been

defined for each month in your organization's fiscal calendar.

Common methods of defining a fiscal pattern include:

- 445, 445, 445, 445 This method is the default fiscal pattern and follows the most

common breakdown: years are broken into quarters, quarters into thirteen weeks (two

four-week months followed by a single five-week month), all anchored to a specific date in

the fiscal calendar.

- 454, 454, 454, 454 This method is common in retail accounting and it helps to

maintain consistent patterns for weekends and holidays across reporting periods and months

across reporting years. Every month within this fiscal pattern begins on a Sunday and ends

on a Saturday. Every month across the pattern (year-to-year) is identical. A retail

accounting fiscal pattern typically configures its calendar to begin on the first Sunday

in February.

- 544, 544, 544, 544 This method is a variation on the 445 fiscal pattern. Each

quarter is divided into thirteen weeks (a single five-week month followed by two four-week

months).

- 4444, 444, 444, 444 This method uses thirteen fiscal periods instead of four

fiscal quarters. Each period has four weeks; each week has seven days. One advantage of

using this fiscal pattern is that every reporting period is identical. One disadvantage of

using this fiscal pattern is that it does not contain fiscal quarters, which are a

requirement for some types of financial reporting methods.

Some examples:

- A typical fiscal pattern:

445,445,445,445

- A fiscal pattern that includes 13 periods:

4444,444,444,444

- A multi-year fiscal pattern. In this example, the fiscal year is configured to begin on

the first Saturday in February, repeats, and then catches the extra week in January during

the fifth year:

445,445,445,445

445,445,445,445

445,445,445,445

445,445,445,445

445,445,445,446

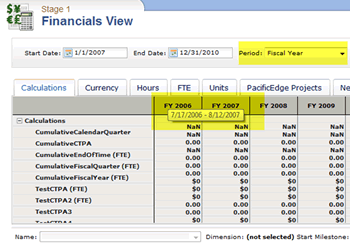

When a fiscal pattern is applied to your organization's fiscal calendar, users will be able

to view the date range defined by the fiscal pattern in areas where fiscal dates are visible,

such as in the Financials tab in the Projects module. Hovering over a date column in

a grid will show the date range that is being used to define the fiscal year being shown. For

example:

Copyright © 2003–2009 Serena Software, Inc. All rights reserved.